Gerechtshof Amsterdam, 23-06-2021, ECLI:NL:GHAMS:2021:1837, 200.275.461/01 OK

Gerechtshof Amsterdam, 23-06-2021, ECLI:NL:GHAMS:2021:1837, 200.275.461/01 OK

Gegevens

- Instantie

- Gerechtshof Amsterdam

- Datum uitspraak

- 23 juni 2021

- Datum publicatie

- 24 juni 2021

- ECLI

- ECLI:NL:GHAMS:2021:1837

- Zaaknummer

- 200.275.461/01 OK

Inhoudsindicatie

OK; enquêterecht; afwijzing van het verzoek tot ontheffing van de OK-bestuurder en, bij wijze van onmiddellijke voorzieningen, tot schorsing van twee bestuurders en tot benoeming van een OK-bestuurder die tot opdracht zal hebben regelmatig verslag uit te brengen

Uitspraak

beschikking

___________________________________________________________________

GERECHTSHOF AMSTERDAM

ONDERNEMINGSKAMER

zaaknummer: 200.275.461/02 OK

beschikking van de Ondernemingskamer van 23 juni 2021

inzake

de besloten vennootschap met beperkte aansprakelijkheid

EXEM ENERGY B.V.,

gevestigd te Amsterdam,

VERZOEKSTER,

advocaten: mr. J.W. Leedekerken, mr. A.P. Koburg en mr. C.N. van Dooren, kantoorhoudende te Amsterdam,

t e g e n

1. de besloten vennootschap met beperkte aansprakelijkheid

ESPERAZA HOLDING B.V.,

gevestigd te Amsterdam,

2. DR. MR. C.B. SCHUTTE,

kantoorhoudende te Amsterdam,

VERWEERDERS,

advocaten: mr. C.B. Schutte, mr. L. Heide-Jørgensen en mr. J. Geertsma, kantoorhoudende te Amsterdam,

e n t e g e n

1. de vennootschap naar vreemd recht

SOCIEDADE NACIONAL DE COMBUSTÍVEIS DE ANGOLA – SONANGOL E.P.,

gevestigd te Luanda, Angola,

2. [A],

wonende te [....] ,

3. [B],

wonende te [....] ,

BELANGHEBBENDEN,

advocaten: mr. M.J. Drop, mr. C. Boersma en mr. R.H. Broekhuijsen, kantoorhoudende te Amsterdam,

e n

wonende te [....] ,

BELANGHEBBENDE,

advocaten: mr. T.S. Jansen en mr. A.S. van der Heide, kantoorhoudende te Amsterdam.

1 Het verloop van het geding

In het vervolg zullen partijen (ook) als volgt worden aangeduid:

- -

-

verzoekster met Exem;

- -

-

verweerster sub 1 met Esperaza;

- -

-

verweerder sub 2 met Schutte;

- -

-

verweerders gezamenlijk met Esperaza c.s.;

- -

-

belanghebbende sub 1 met Sonangol;

- -

-

belanghebbende sub 2 met [A] ;

- -

-

belanghebbende sub 3 met [B] ;

- -

-

belanghebbenden sub 1, 2, en 3 gezamenlijk met Sonangol c.s.;

- -

-

belanghebbende sub 4 met [C] .

De Ondernemingskamer heeft bij beschikkingen van 17 september 2020 en 22 september 2020 – zakelijk weergegeven – een onderzoek bevolen naar het beleid en de gang van zaken van Esperaza over de periode vanaf 1 januari 2017, mr. W.J.M. van Andel (hierna: mr. Van Andel) benoemd als onderzoeker, alsmede – bij wijze van onmiddellijke voorziening – [C] geschorst als bestuurder van Esperaza, Schutte benoemd tot zelfstandig bevoegd bestuurder met beslissende stem, de door Exem gehouden aandelen in Esperaza ten titel van beheer overgedragen aan mr. J.R. Berkenbosch (hierna: mr. Berkenbosch) als beheerder van die aandelen. Bij beschikking van 18 januari 2021 heeft de Ondernemingskamer het bedrag dat het onderzoek ten hoogste mag kosten vastgesteld op € 150.000, exclusief btw.

Exem heeft bij op 21 mei 2021 ingekomen verzoekschrift met producties de Ondernemingskamer verzocht, bij beschikking uitvoerbaar bij voorraad, (i) Schutte met onmiddellijke ingang te ontheffen uit zijn functie als tijdelijk bestuurder van Esperaza en, bij wijze van onmiddellijke voorzieningen voor de duur van het geding, (ii) [A] en [B] te schorsen als bestuurders van Esperaza en (iii) een nader aan te wijzen persoon te benoemen tot zelfstandig bevoegd bestuurder van Esperaza, met veroordeling van Esperaza in de kosten van het geding.

Op verzoek van de Ondernemingskamer heeft Schutte bij e-mail met bijlagen van 25 mei 2021 meegedeeld welke handelingen hij als bestuurder van Esperaza voornemens is te verrichten die (kunnen) raken aan de positie van Exem als (beweerdelijk) aandeelhouder van Esperaza.

Exem heeft bij op 28 mei 2021 ingekomen nader verzoekschrift, met producties, verzocht om, in aanvulling op haar eerdere verzoek, bij wijze van onmiddellijke voorziening voor de duur van het geding, (iv) de door de Ondernemingskamer te benoemen nieuwe zelfstandig bevoegd bestuurder van Esperaza op te dragen regelmatig verslag uit te brengen aan de Ondernemingskamer en de door de Ondernemingskamer benoemde beheerder van aandelen.

Esperaza c.s. hebben bij op 9 juni 2021 ingekomen verweerschrift met producties de Ondernemingskamer verzocht Exem niet ontvankelijk te verklaren in haar verzoek, althans dit af te wijzen, met veroordeling van Exem in de kosten van het geding, uitvoerbaar bij voorraad.

Sonangol c.s. hebben bij op 10 juni 2021 ingekomen verweerschrift met producties de Ondernemingskamer verzocht het verzoek van Exem af te wijzen en, uitvoerbaar bij voorraad, Exem te veroordelen in de kosten van het geding.

[C] heeft bij op 10 juni 2021 ingekomen verweerschrift met producties de Ondernemingskamer verzocht bij beschikking, uitvoerbaar bij voorraad, het verzoek van Exem toe te wijzen.

Het verzoek is behandeld ter openbare terechtzitting van de Ondernemingskamer van 17 juni 2021. Bij die gelegenheid hebben mrs. Leedekerken, Jansen, Geertsma, Schutte, Drop en Broekhuijsen de standpunten van de onderscheiden partijen toegelicht aan de hand van – aan de Ondernemingskamer en de wederpartijen overgelegde – aantekeningen. Van de zijde van Exem en Sonangol c.s. zijn op voorhand aan de Ondernemingskamer en de wederpartijen gezonden nadere producties overgelegd. Verder heeft mr. Berkenbosch zijn standpunt toegelicht aan de hand van – aan de Ondernemingskamer en de wederpartijen overgelegde – aantekeningen. Partijen en hun advocaten hebben vragen van de Ondernemingskamer beantwoord en inlichtingen verstrekt.

2 De feiten

De Ondernemingskamer gaat, in aanvulling op de hetgeen in de beschikking van 17 september 2020 is overwogen, uit van de volgende feiten:

[D] , die in 2016 geregistreerd stond als Ultimate Beneficial Owner van Exem (zie r.o. 2.4 van de beschikking van 17 september 2020), is op 29 oktober 2020 overleden.

Bij brief van 4 mei 2021 heeft Schutte aan Sonangol, Exem en [C] een door hem opgesteld (concept)rapport toegestuurd getiteld “Assessment of Exem Energy B.V.’s Claimed Interest in Esperaza Holding B.V.” (hierna ook: de assessment). In de brief schrijft Schutte – kort gezegd – dat het aandeelhouderschap van Exem onderwerp is van arbitrageprocedures tussen Exem en Sonangol, waarbij Esperaza geen partij is; dat de legitimiteit van de verwerving van die aandelen door Exem onderwerp is van onderzoek door de autoriteiten in zowel Nederland als in het buitenland; dat hij onderzoek heeft gedaan naar de boeken en bescheiden van de vennootschap; dat hij zijn bevindingen heeft besproken met zijn medebestuurders [A] en [B] en dat hij deze bevindingen heeft vastgelegd in de assessment; dat hij op basis daarvan vermoedt dat het beweerde belang van Exem in Esperaza het resultaat is van corrupte transacties; dat alle transacties, besluiten en rechtshandelingen die het resultaat of gevolg zijn van illegale activiteiten nietig zijn op grond van artikel 3:40 lid 1 BW en dat om die reden Esperaza het beweerde belang van Exem in Esperaza niet langer kan en mag erkennen of faciliteren. Schutte verzoekt Sonangol, Exem en [C] om uiterlijk 18 mei 2021 hun eventueel commentaar op zijn bevindingen in de assessment kenbaar te maken en verzoekt Exem om in dat kader ook mee te delen wie haar Ultimate Beneficial Owner(s) (hierna: UBO(s)) is of zijn en dat met bescheiden te staven.

De assessment houdt – voor zover hier van belang – het volgende in:

“1. BACKGROUND AND PURPOSE OF THIS REPORT

My Appointment and Responsibilities

(...) In its decision of 22 September 2020 (ECLI:NL:GHAMS:2020:2515), the Enterprise Chamber appointed me as the director with a decisive vote within the board and with plenipotentiary powers to represent the Company (...).

I note that the Enterprise Chamber restricted the scope of the inquiry by the Investigator to the facts described in the 17 September 2020 decision over the period as of 1 January 2017. I also note that Exem and Sonangol are parties to various arbitrations conducted under the rules of the Netherlands Arbitration Institute, which are still pending at this moment (“the Arbitrations”). From the information provided to the Enterprise Chamber and noted in its 17 September 2020 decision (vide consideration 2.29), the most far-reaching pending Arbitration (NAI case No. 4687) concerns, inter alia, Sonangol’s allegation that Exem’s acquisition in 2006 of its 40% share in the Company is null and void under the applicable Dutch law for being the fruit of corruption.

I note that the Company is not a party to any of the Arbitrations. In consequence, the arbitral awards of the Arbitrations will not bind the Company and will not necessarily cause legal effects the Company must acknowledge or abide. I further note that very serious suspicions and allegations have been raised against Exem and its ultimate beneficial owner or owners, which have led to opening criminal investigations and/or prosecution in various jurisdictions, including the Netherlands. In that context, the Public Prosecutor issued his aforementioned freezing order regarding the shares purportedly held by Exem and the Enterprise Chamber handed down its decision appointing me.

As a newly appointed director, I have my own responsibility to conduct my own, independent review and draw my own legal conclusions as regards to the suspicions concerning the legal situation the Company is in and its position regarding the interests Exem claims to hold in the Company. As the Company has been controlled, until my appointment, by persons related to Exem, I have realized that the past financial statements of the Company may have been affected by and reflect transactions that are dubious and need reassessment. Any illegalities I may find, must and will be addressed and, where necessary, will be amended in future financial statements.

To that end, I have examined the Company’s administration and available documentation, including legal arguments and exhibits of both Sonangol and Exem submitted to the Enterprise Chamber. In this report, I lay down my observations, assessments and legal conclusions, which will be the basis for the actions I intend to undertake to address the situation and restore the rightful economic reality where necessary.

Object of the Review and Questions

I have first made an inventory of all interests Exem claims to have in the Company, based on its financial statements.

According to the financial statements of the Company since 2006, Exem has 7,280 shares (40% of the share capital) in the Company. The basis for this representation has been a transaction notarized by deed of transfer dated 29 December 2006 according to which these shares were transferred by Sonangol to Exem on that date (“the Exem Transaction”).

According to the financial statements of the Company since 2010, Exem has a claim of

€ 4,180,377 against the Company under an interest free loan (“the Exem Loan”). The basis for this is a document titled ‘Loan Agreement’ dated June 2009 without a specific date (“the Loan Agreement”). I have found no other financial interests of Exem in the Company. (...)

The first question for my review concerns the cause (Dutch: titel) of the Exem Transaction respectively the Exem Loan. If that cause is non-existent and/or null and void (Dutch: nietig), the conclusion must be that the Company has been reporting a shareholding and a loan in favor of Exem for many years without a legal basis. My assessment of the facts is reported in Chapter 2.

If my conclusion is that the causes of the Exem Transaction and the Exem Loan are null and void respectively non-existent, the necessary following questions are what legal consequences follow from this conclusion and what the Company must do under the circumstances. I shall respond to these questions and summarize the actions I intend to undertake in Chapter 3.

2 2. ASSESSMENT OF THE FACTS

Scope, decision process and standard of proof

(...) The fact that I have been judicially appointed does not imply that I am to conduct my assessment of the facts as a judicial authority. It is settled case-law of the Enterprise Chamber, that a director appointed by that court has the same powers and the same responsibilities as any other director (Dutch: bestuurder) as laid down in the Dutch Civil Code (“DCC”) and other Dutch private law. This means that neither the Company nor I have the obligation to establish facts, if they should be controversial, in accordance with the procedures and standards of a court of law.

I am a director, not a judge, and must act in the interest of the Company at all times. In this particular case, I have come to the compelling conclusion that that interest is to give immediate effect to my conclusions, given the extreme seriousness of the facts at hand, which are also already the object of criminal investigations in various jurisdictions and which are barring the Company from conducting its ordinary business even as regards to the most daily issues, such as administering a bank account. In this context, I must also note that the standard of proof by which I am guided in my legal assessment as a director of the Company, is not the ‘beyond reasonable doubt’ test. (...) As a director who must take decisions on the basis of available information measuring the probabilities of the facts and balancing those probabilities with the risks and interests of the Company, I can and must restrict my analysis to the information before me. Where the documentation of the Company might be obscure and where Exem may dispute certain facts, I shall base my conclusions on what I consider to be probable (Dutch: aannemelijk) in light of all information that a company board can reasonably be expected to collect and examine to establish facts and circumstances according to the criteria of reasonableness and equity (Dutch: naar maatstaven van redelijkheid en billijkheid). In any event, I have restricted my analysis on information that is uncontroversial because it is based on public documents, such as notarial deeds, and/or because it is common ground or relied upon by Exem in the parties’ allegations before the Enterprise Chamber.

In sum, the guiding principle for me to find and assess the facts in this matter is therefore not the due process standard to which courts are subject, but the question whether a reasonable acting company board can – and, in the affirmative, in light of its responsibilities under the circumstances: must – conclude that Exem’s acquisitions of the Exem Shares and the Exem Loan are based on causes that are non-existing or null and void, and that the Company must act accordingly.

Basic Facts

All or most of the following facts are either common ground or uncontroversial in light of the documents:

(i) According to a notarial deed of transfer dated 6 December 2005, the Dutch private company ABN AMRO Special Corporate Services B.V. transferred all 40,000 shares in the share capital of the Company, numbered 1 through 40,000, each having a value of one Dutch guilder (after conversion: € 0.45) to the Portuguese public company Amorim Holding II SGPS, S.A. (formerly known as Financiamentos Mobiliarios SGPS S.A.). Reference is made to a share purchase agreement of 6 December 2005 and the purchase price was € 24,151.21.

(ii) According to a notarial deed of amendment of the articles of association of the Company dated 13 December 2005, all 40,000 shares in the share capital of the Company were converted into 18,200 shares in the share capital of the Company, numbered 1 through 18,200, each share having a par value of one euro (€ 1.00), together constituting the entire issued capital of the Company.

(iii) The Company acquired the 45% shareholding in Amorim Energia B.V. (“AEBV”) before 30 January 2006.

(iv) According to a notarial deed of transfer dated 30 January 2006, Amorim Holding II SGPS, S.A. transferred all its 18,200 shares in the share capital of the Company to Sonangol. Reference is made to a share purchase agreement dated 20 December 2005 (Annex I) and a confirmation statement (Annex II). The purchase price amounted to € 18,200. The share purchase agreement refers to a letter of Amorim Holding II, SGPS, S.A. to Sonangol dated 20 December 2005, which sets out the joint venture agreement between these companies to acquire shares in the public company incorporated under Portuguese law Galp Energia, SGPS, S.A. (“Galp”) through AEBV and to then make an IPO in Lisbon’s stock market in the course of 2006. That letter is signed for its approval on behalf of Sonangol by its then chairman of the board of directors, [E] (“[E]”). The letter makes no mention of Exem and/or its ultimate beneficial owners as envisaged participant in the structure, or in any other way whatsoever.

(v) According to the 2006 financial statements, Sonangol made a total contribution to the Company by way of share premium of € 187,689,700 and lent € 5,775,224 to the Company.

(vi) According to the 2006 ledger of the Company, the Company made a first contribution to AEBV by way of share premium of € 81,052,250 on 30 January 2006.

(vii) In the administration of the Company, there is a document titled “Written statement by the sole shareholder of Esperaza Holding B.V.” dated 26 July 2006, signed on behalf of Sonangol by [E] as its chairman of the board of directors. In the recitals of the written statement, it is mentioned that it was Sonangol’s intention to hold the share capital in the Company through a Malaysian subsidiary of Sonangol, that Sonangol was holding the Company only temporarily and that Sonangol envisaged to establish the Malaysian company shortly and to transfer immediately “the entire share capital of the Company” to the Malaysian company. In light of those considerations, [E] confirmed on behalf of Sonangol: “that it has always been its intention to hold its shares in the Company through a Malaysian subsidiary of Sonangol and that such Malaysian company is currently being established”.

(viii) According to the 2006 ledger of the Company, the Company made a second contribution to AEBV by way of share premium of € 107,947,675 on 14 August 2006.

(ix) AEBV acquired, also with the funds received from the Company, shares in Galp, in total 276.472.161 shares with voting rights, representing 33.34% of the total share capital of Galp before its IPO. This is also the share AEBV holds currently in Galp.

(x) On 23 October 2006, Galp successfully concluded its IPO and its share was listed at the stock exchange Euronext Lisbon. Its opening price was € 5.910.

(xi) According to a notarial deed of transfer dated 29 December 2006 (notary (...) (Stibbe)), Sonangol transferred 7,280 shares in the capital of the Company, numbered 10,921 to 18,200, to Exem, i.e. the Exem Transaction. Sonangol, Exem and the Company were all represented by the same proxy, an employee of Stibbe. According to the attached powers of attorney, the Stibbe proxy represented [E] in his capacity “as Chairman of the Board of Directors of Sonangol”, who represented solely Sonangol. Reference is made to a share purchase agreement dated 21 December 2006 (“the Agreement”) and to a purchase price of € 75,075,880, that “will be paid in accordance with the terms and conditions of the Agreement”.

(xii) It is common ground in the proceedings before the Enterprise Chamber, that the “Agreement” referred to in the aforementioned notarial deed of 29 December 2006 is a document with the title Share Purchase Agreement dated 21 December 2006 (“the Exem SPA”).

(xiii) Friday 29 December 2006 was the last trading day of 2006 at the Euronext Lisbon. Galp’s closing price was € 6.940.

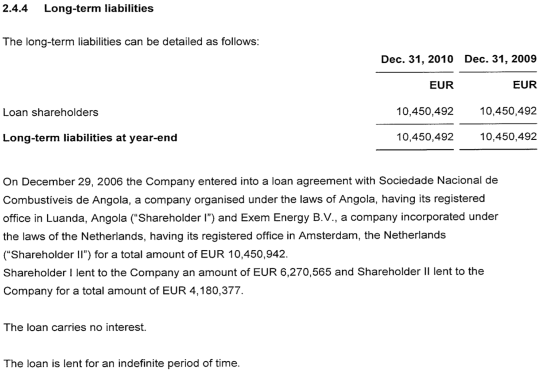

(xiv) In the financial statements of the Company of 2006 to 2008, an interest free loan was recorded in favor of Sonangol as the Company’s creditor for, eventually in 2008, an amount of € 10,450,942.

(xv) The total of share premium contributions (€ 187,689,700) and loans (€ 10,450,942) the Company received, only from Sonangol, amounts to € 198,140,642 (all received in 2006 to 2008); whereas the total share premium contribution of the Company to AEBV amounts to € 197,999,925 (all paid in the period 2006 to 2008).

(xvi) In the financial statements of the Company of 2009 and thereafter, the interest free loan recorded in favor of Sonangol until 2008 was recorded as ‘loan shareholders’ and as of 2010 as split into a loan of € 4,180,377 in favor of Exem, representing 40% of € 10,450,942, and the remainder in favor of Sonangol. A document titled ‘Loan Agreement’ dated 2009 (no specific date) (“Loan Agreement”) specifies that the amount of € 10,450,942 was lent to the Company, out of which € 4,180,377 was lent by Exem and € 6,270,565 by Sonangol. The Loan Agreement is signed by [F] , ‘President SNL Holdings’, on behalf of Sonangol, by [C] on behalf of Exem and by [G] and the same [C] on behalf of the Company.

(xvii) According to a notarial deed of 5 November 2015, the articles of association of the Company were amended (“the 2015 Articles of Association”). According to this amendment, all shares of the Company are either shares A or shares B. The shares numbered 1 to 10,920 were converted into shares A1 to A10,920 respectively. The shares numbered 10,921 to 18,200 were converted into shares B1 to B7,280. All shares continued having the same par value of € 1.00 and the share capital of the Company continued being € 18,200.

(xviii) On 25 September 2017, President [H] left office. During the last years of his office, President [H] appointed [E] as Vice-President of Angola and his daughter [I] as chairwoman of board of directors of Sonangol.

(xix) The new President of Angola, [J] , dismissed [I] as chairwoman of the board of directors of Sonangol on 15 November 2017. Thereafter, the disputes arose between Sonangol and Exem which have resulted in the pending Arbitrations and the petition to the Enterprise Chamber.

Legal framework

Both the Exem SPA and the Exem Transaction are governed by Dutch law. (...) According to the applicable Dutch law, a legal transaction consisting of a transfer of title is null and void if the cause (in Dutch: titel) is null and void. In this case, the Exem SPA constitutes the cause of the Exem Transaction. (...) Sonangol has stated before the Enterprise Chamber that the Exem Transaction is null and void under Article 3:40.1 DCC for being in violation of public morality and public order. (...) As stated above, this argument has also been put forward by Sonangol in the Arbitrations between Sonangol and Exem. (...)

Any juridical act that is incompatible with the principles and values which are considered as fundamental within the Dutch legal order, is against public order. Consequently, if an act aimed at sorting legal effect (Dutch: rechtshandeling, i.e. ‘juridical act’) is governed by Dutch law, that juridical act is null and void if it violates public order. (...)

The compelling nature of the reason for me to assess the facts at hand on my own account and to act accordingly with immediate effect, is also corroborated by the provisions of Dutch criminal law to which the Company is subject. Reference can be made specifically to the public offence of money laundering by fault or culpa (Dutch: schuldwitwassen). Under Article 420quater of the Dutch Criminal Code, the Company may already be in violation of the anti-money laundering laws if, for example, it facilitates giving legitimate appearance to financial interests (Dutch: vermogensrechten) it “must reasonably suspect” (Dutch: “redelijkerwijs moet vermoeden”) to be the result of a criminal offence. (...)

The Exem Transaction, a sale of public property not at arm’s length

(...) My first observation as a director of the Company is that I find the transaction underlying the purchase of 40% of the shares in the Company an extremely unusual transfer of property rights in the Company. Exem obtained a financial advantage through the Exem Transaction that no ordinary person or company could have been expected to obtain under ordinary circumstances. The Exem Transaction is evidently ‘onzakelijk’, i.e. ‘not at arm’s length’, raising serious suspicions as to its legitimacy. My observation is based on the following facts.

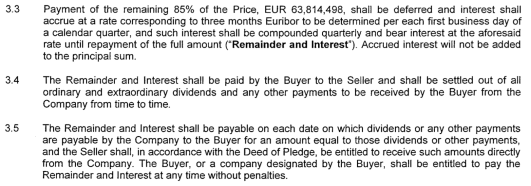

The Exem Transaction of 29 December 2006 is characterized by the following stipulations as per the Exem SPA of 21 December 2006:

1. Exem purchased 40% of the Company’s share capital from Sonangol.

2. The purchase price was set at € 75,075,880.

3. Exem was to pay 15% of the purchase price, i.e. € 11,261,382, prior to the transfer

of the shares.

4. As regards to the remaining 85% of the purchase price, the Exem SPA reads:

5. As regards to the period of repayment, Article 3.7 reads:

6. According to Article 3.8, the following security is provided by Exem to Sonangol:

In order to assess whether this purchase price was at arm’s length (Dutch: zakelijk), I consider the following financials regarding Sonangol’s investment in the Company as relevant:

a) The Company had made two share premium contributions to Amorim Energia B.V. in 2006, one of € 81,052,250 on 30 January 2006 and another one of € 107,947,675 on 14 August 2006, i.e. in total € 188,999,925.

A 40% stake of this amount would be: € 75,599,970.

b) At the time of the Exem Transaction, Sonangol had made the following

investments in the Company:

- Purchase price paid to Amorim for the Company: € 18,200

- Share premium contributions total: € 187,689,700

- Long-term interest free loan (quasi share premium): € 5,775,22412

Thus, Sonangol’s total investment on 29 December 2006 amounted to € 193,483,124.

A 40% stake of this amount would be: € 77,393,350.

c) On 29 December 2006, the value of Esperaza’s share in AEBV was € 289,624,236.

The equity of Esperaza was € 288,275,659.

A 40% stake of this amount would be: € 115,310,264.

These numbers show that Exem obtained an asset that was worth € 115,310,264 on 29 December 2006, paying an effective consideration of € 11,261,382 and assuming a longterm debt of € 63,814,498. This disproportion already makes the transaction more than questionable.

I understand that there is discussion between Sonangol and Exem as to whether the payment of € 11,261,382 was done with funds obtained from a licit origin. Indeed, I note that the evidence of this payment submitted by Exem in the proceedings before the Enterprise Chamber does not refer to a payment by Exem itself but by some off-shore company called Exem Africa Limited. (...) Even if I am to assume that the payment of € 11,261,382 was made and that this was done with legitimate funds, there can be no doubt that the Exem SPA (which was also signed on behalf of the Company) is far from being an agreement at arm’s length. In fact, the way in which the Exem SPA has been worded with expressions that make it look as though it were at arm’s length, evidence that the instrument is a travesty of a legitimate transaction. The represented rationale does not resist any possible legal-economic analysis.

According to that transaction, Sonangol transfers ownership of an asset on 29 December 2006, which has an objective value of € 115,310,264 at that date. The objectivity of that value cannot be contested, as the Company’s assets exclusively consist of high yielding shares it is holding through AEBV in the company Galp, which had been successfully launched as a listed company on 23 October 2006. Exem receives this value in return for a payment of € 11,261,382 and a promise to pay € 63,814,498 plus a three months Euribor interest rate without providing any further guarantee to Sonangol than the shares themselves.

Economically this boils down to Exem’s purchasing Galp shares at a tenth of their market value, with the promise that if the Galp shares will yield sufficient dividend within 10 years, Exem will pay another half of their 2006 value plus a three months Euribor interest. This cannot be characterized as a usual share transaction. This is a transfer of an extremely valuable financial asset by a publicly owned entity to a privately owned entity, without receiving consideration that is even closely proportional to the value of that asset. Exem pays less than 10% of the Galp share price and runs no further risk in case the Galp share price should drop. If the Galp share increases in price and yields dividends, all advantages are solely for Exem. Exem may choose to pay another 50% of the 29 December 2006 value plus interest if it wishes to keep the shares after 2017.

First, the interest of three months Euribor cannot be deemed to be at arm’s length in the absence of any additional risk margin, surplus or spread (Dutch: opslag). Euribor is short for Euro Interbank Offered Rate and is the rate European banks charge each other on the loans between them. It is used as a reference rate for loans between other economic entities and the Euribor rate will then be increased with a risk surplus depending on the personal circumstances of the borrower (insolvency risk) and the securities offered. Exem is obviously neither a regulated European bank nor does it have the low-risk profile that pertains to a European bank. Exem is no more than a Dutch holding company and there is no indication that Exem can offer any reasonable recourse for this loan. This interest rate is therefore not at arm’s length, being as it is extraordinarily favorable for Exem.

Further, the Company shares that Exem pledges to Sonangol may look like but are no real security: if the Galp share price drops to zero, the Company share value drops to zero and Sonangol’s security becomes worthless. In that case, Sonangol would never have received more than € 11,261,382 for a share that at the time of the Exem Transaction had a value of € 115,310,264. The same applies if Exem does not fulfill its payment obligations: there is no indication that Sonangol could get paid more than the € 11,261,382 from Exem itself. This means overall that Sonangol has no security that it would effectively ever receive more than the initial € 11,261,382 from Exem itself, i.e. less than 10% of the value of the asset according to the objective market value of the underlying Galp shares.

In sum, there is only an upside for Exem and the downside is only for Sonangol. Exem basically bought Galp shares for less than 10% of their market value, with the option that if Exem should want to keep them after 10 years, it would have to pay an additional 50% of the 2006 price. This boils down to investing in listed stocks at a 90% discount and speculating with the shares at the seller’s risk and with still another 40% discount.

Apparently, Exem understands that the consideration contemplated in the Exem SPA does not make economic sense if one looks at the underlying values on 29 December 2006. In its defense, Exem explained that the agreed price was connected to the price Sonangol agreed to pay to Amorim earlier that year, when the value of the Galp shares was not as certain yet. In that view, Exem was sharing in the risk of the Galp IPO.

In order to substantiate that argument, Exem submitted a document titled ‘Memorandum of Understanding’, on its face signed on 25 January 2006 by [E] on behalf of Sonangol and a [K] ‘Attorney’, on behalf of Exem Africa Limited, “a company incorporated in British Virgin Island” (sic). There is discussion between Sonangol and Exem about the authenticity of this document, especially as regards to its date. I observe that there is good reason to believe that the date of the document is not correct and that the document overall is not in accordance with the facts as they should be legally, i.e. vis-à-vis the outside world including the public authorities. The document is in open contradiction with [E] ’s statement of 26 July 2006 referred to above under (vii) of the basic facts.

Yet, even if I assume that this agreement was already in place in January 2006 as its text suggests and that it was entered into in good faith, the fact is that it does not convert the Exem Transaction into one that was at arm’s length. In fact, the Memorandum of Understanding (if truthful) implies that Exem was actually left at liberty to speculate on the Galp IPO with no cost or risk. For, if there was an agreement already in January 2006 – i.e. before Sonangol was to invest €188 million in AEBV through the Company – to have Exem pay € 11 million, it confirms that Exem was allowed to speculate with Sonangol’s money and for Sonangol’s risk, as Exem was not asked to actually pay out the €11 million until December 2006 – i.e. after it was clear the Galp IPO on 23 October 2006 had been a success and the payment of € 11 million was less than 10% of the actual market value at that time. The Memorandum of Understanding (if truthful) confirms that the entire speculation during 2006 was done at Sonangol’s risk, whereas the upside was entirely for Exem: there is, again, no mechanism or guarantee in the agreement that would allow Sonangol to effectively enforce its claim to get the agreed price paid from Exem if things had gone wrong with the IPO.

In sum, the conclusion must be that the Exem SPA was ‘onzakelijk’ (i.e. does not meet the at arm’s length test), granting a very substantial and considerable advantage to Exem effectively constituting a gift or favor granted by [E] on behalf of Sonangol to the detriment of Sonangol’s property. Exem and thus its ultimate beneficial owner or owners obtained very valuable public property which Sonangol lost without receiving closely proportional consideration. Consequently, the Exem Transaction constituted an unusual transfer of public property to Exem that raises reasonable suspicions.

The Exem Transaction, an evidently illicit transaction

As regards to the background of Exem and the decision making of Sonangol to enter into the Exem SPA and co-operate with the Exem Transaction, the following facts have transpired:

1. Exem’s ultimate beneficial owner at the time of the Exem SPA and Exem Transaction was [D] and, allegedly, also his wife [I] .

2. [I] is the daughter and her late husband [D] was the son-in-law of [H] . According to public sources, [I] and [D] were married from 2002 until [D] ’s death on 29 October 2020.

3. [H] was President of Angola from 1979 to 2017.

4. Both the articles of association of Sonangol and the appointment of its board members were discretionary decisions of the President of Angola.

5. Accordingly, [E] , who represented Sonangol in the Exem SPA and the Exem Transaction in 2006, had been appointed chairman of the board of directors of Sonangol by President [H] .

6. I have seen no evidence that the Exem SPA and Exem Transaction were officially disclosed to, let alone approved by, the board of directors of Sonangol and/or its sole shareholder, the Republic of Angola.

7. I have seen no evidence that there was any transparency or democratic and/or independent control or assessment, let alone approval, as regards to [E] ’s decision to enter into the Exem SPA and Exem Transaction on behalf of Sonangol.

8. During the last years of his office, President [H] appointed [E] as Vice-President of Angola and his daughter [I] as chairwoman of the board of directors of Sonangol.

9. The new President of Angola, [J] , dismissed [I] as chairwoman of the board of directors of Sonangol on 15 November 2017, around two months after succeeding President [H] in office.

Thereafter, the disputes arose between Sonangol and Exem which have resulted in the pending Arbitrations and the petition to the Enterprise Chamber, in which Sonangol denounced the illicit nature of the transactions concerning Exem’s interest in Sonangol. As regards to the lack of transparency surrounding and following the Exem Transaction, I have taken note of the following facts:

1. Exem also gained controlling powers over the Company by way of contractual and corporate instruments signed by [E] on behalf of Sonangol on the one hand and Exem and the Company on the other hand, such as a Shareholders’ Agreement dated 21 December 2006. This de facto control only came to an end with the 17 and 22 September 2020 decisions of the Enterprise Chamber.

2. The Exem SPA and other documents referring to the relationship between Sonangol and Exem, including the aforementioned Shareholders’ Agreement dated 21 December 2006, explicitly stipulate the confidentiality of the agreements. In this respect, Clause 9.1 of the aforementioned Memorandum of Understanding dated 25 January 2006, whose authenticity is disputed by Sonangol but defended and relied upon by Exem, deserves special attention:

3. Exem’s purported interest in Esperaza became public only after the so-called Luanda Leaks were published by the International Consortium of Investigative Journalists in January 2020.

In sum, I observe that the Exem SPA and Exem Transaction were signed on behalf of Sonangol and the Company at a period that Sonangol, the Company and Exem were all three under indirect control of the then President of Angola respectively his family members. I further observe that Exem’s control over the Company was not made public. The contractual confidentiality clauses and the interposing of Exem and its holding company as front companies avoided that Exem’s ultimate beneficial owner or owners belonging to the Presidential family were made public.

The above combination of uncontroversial facts provides sufficient ground for me to conclude that the Exem Transaction constitutes a transaction aimed at secretly transferring Angolan public property into the private estate of family members of the former President of Angola on economically unsound grounds. This transfer was evidently to the advantage of the family and to the detriment of the Republic of Angola, and intended to be kept secret.

Conclusion regarding the Exem Transaction

I conclude that this transfer of public property to family members of the former President of Angola through a transaction that was concealed from the public and which implies the transfer of publicly owned assets of a very high value into their private estates in return for economically unsound consideration, evidences that the Exem Transaction is itself, or is part of, an act of corruption and money laundering scheme. I note that the same complex of facts may also constitute public offences such as bribery, embezzlement, money laundering and/or other criminal offences. This is for the Public Prosecutor to assess.

The ongoing investigations, which have not yet concluded, do not preclude me from concluding and having to conclude that the Exem SPA and its intended property transfer by way of the Exem Transaction are illicit (onoorbaar) for being in violation of public morality and public order. As the Exem SPA and Exem Transaction are ruled by Dutch private law, my conclusion is that both the Exem SPA and, consequently, the Exem Transaction are null and void under Article 3:40.1 DCC for being against international and Dutch public order. Consequently, this also implies that no conduct, act, deed or instrument aimed at legitimating or facilitating the Exem SPA and Exem Transaction can sort any legal effect whatsoever within the Dutch legal order. These conclusions are inescapable for me on the basis of my assessment and require immediate further action in light of the very serious facts at hand.

Legal assessment and conclusion regarding the Exem Loan

The other interest Exem claims to have in the Company is the Exem Loan, recorded in the Company’s annual accounts since 2010. The legal basis for the Exem Loan is the Loan Agreement of June 2009 (without a specific date). According to its Clause 7.1, the Loan Agreement is governed by Dutch law. According to the recitals of the Loan Agreement, Sonangol and Exem entered into a verbal loan agreement on 29 December 2006, pursuant to which they granted an interest free loan of € 10,450,942 to the Company, 40% of which (€ 4,180,377) was lent by Exem when it became the 40% shareholder of the Company on that same 29 December 2006.

According to the 2006 and 2007 Company ledgers, the loan was paid by Sonangol to the Company. The annual accounts of the Company until 2008, mention that this loan was a ‘loan shareholder’ (singular) to the Company. Only as of the annual accounts of 2009, 40% of the loan was reported to have been assigned to Exem and the accounts started to mention the loan as a ‘loan shareholders’ (plural). According to the ledger, the loan was split per 1 January 2010 in favor of Exem. In the 2010 annual accounts, an explanation was added (...) which reads as follows:

There is no indication in the Loan Agreement, in the annual accounts or anywhere else in the Company’s administration of a cause (Dutch: titel) for this partial assignment of Sonangol’s loan to Exem. Neither is there any evidence of any consideration Exem paid for that assignment or of any funds transferred by Exem to the Company justifying the Exem Loan according to the Loan Agreement. I further note that the Loan Agreement was signed by Sonangol and the Company at a period that Sonangol, the Company and Exem were all three under indirect control of the then President of Angola respectively his family members. In light of this all, there are serious doubts as to the truthfulness of the Loan Agreement.

Yet, I need not to examine that aspect here further, as the document cannot sort any legal effects even if it were to be assumed to be genuine. Such for the following reasons. To the extent that the cause was also the Exem SPA and Exem Transaction, as the recitals of the Loan Agreement imply, this assignment follows their same fate and is also null and void under Article 3:40.1 DCC. In the absence of any other evidence of a cause or consideration, the Exem Loan must be considered non-existent under Article 3:84.1 DCC. Either way, there is no, de iure, Exem Loan against the Company.

In conclusion, the Company must consider Sonangol the sole lender of the total loan recorded in the annual accounts and this must be amended accordingly in the next accounts.